The global Outsourced Semiconductor Assembly and Test (OSAT) industry serves as the essential backend layer of the semiconductor supply chain by transforming finished silicon wafers into packaged, tested, and qualified chips through a suite of processes known as Assembly, Test, Mark, Package (ATMP). Reflecting a steady recovery and growth trajectory, the combined revenue of the world's top 10 OSAT companies reached USD 41.56 billion in 2024, up 3% year-on-year. Building upon our foundational industry tracking since the release of our first Top OSAT Players ranking in April 2019, this updated list reflects the latest shifting dynamics, which are covered in comprehensive detail within our premium report.

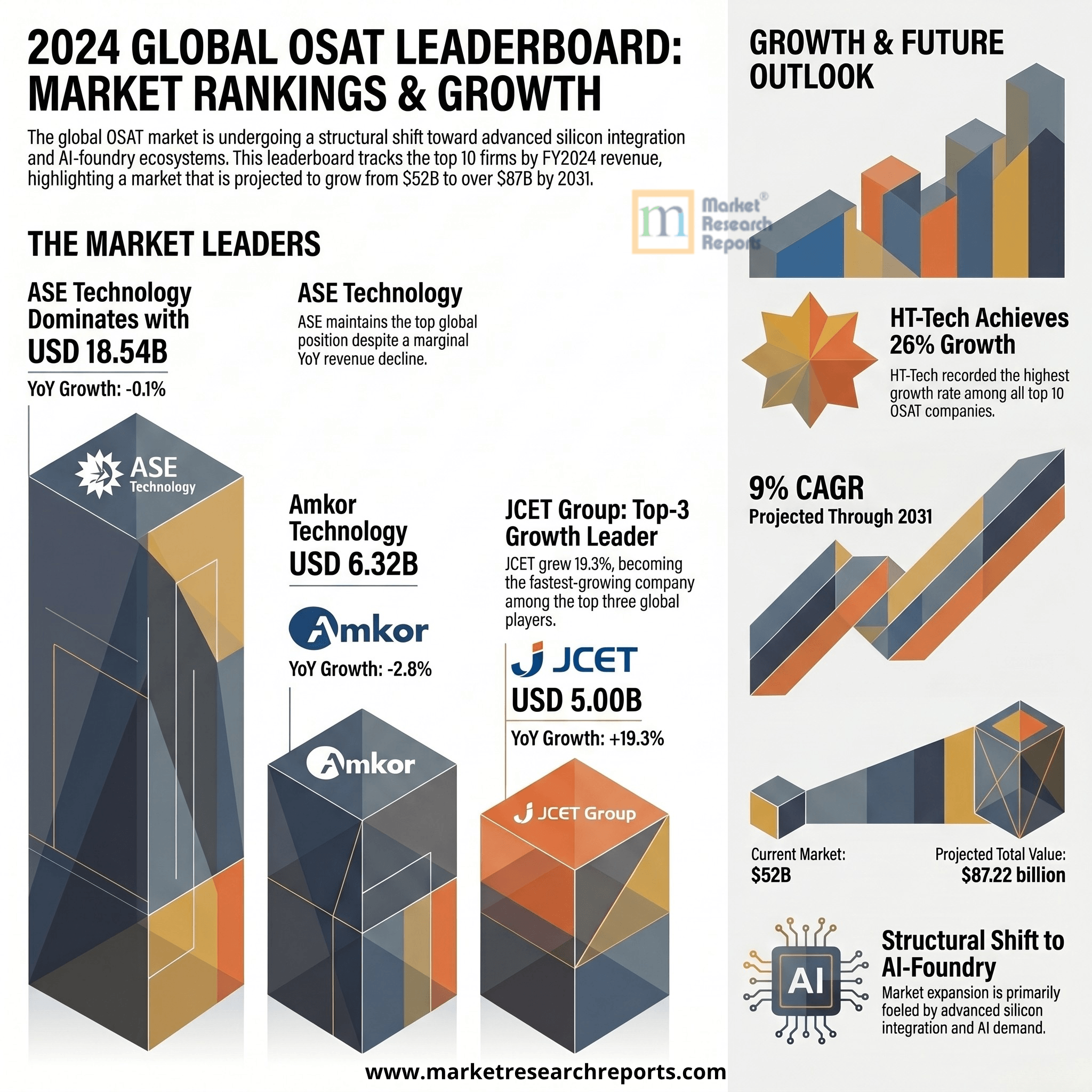

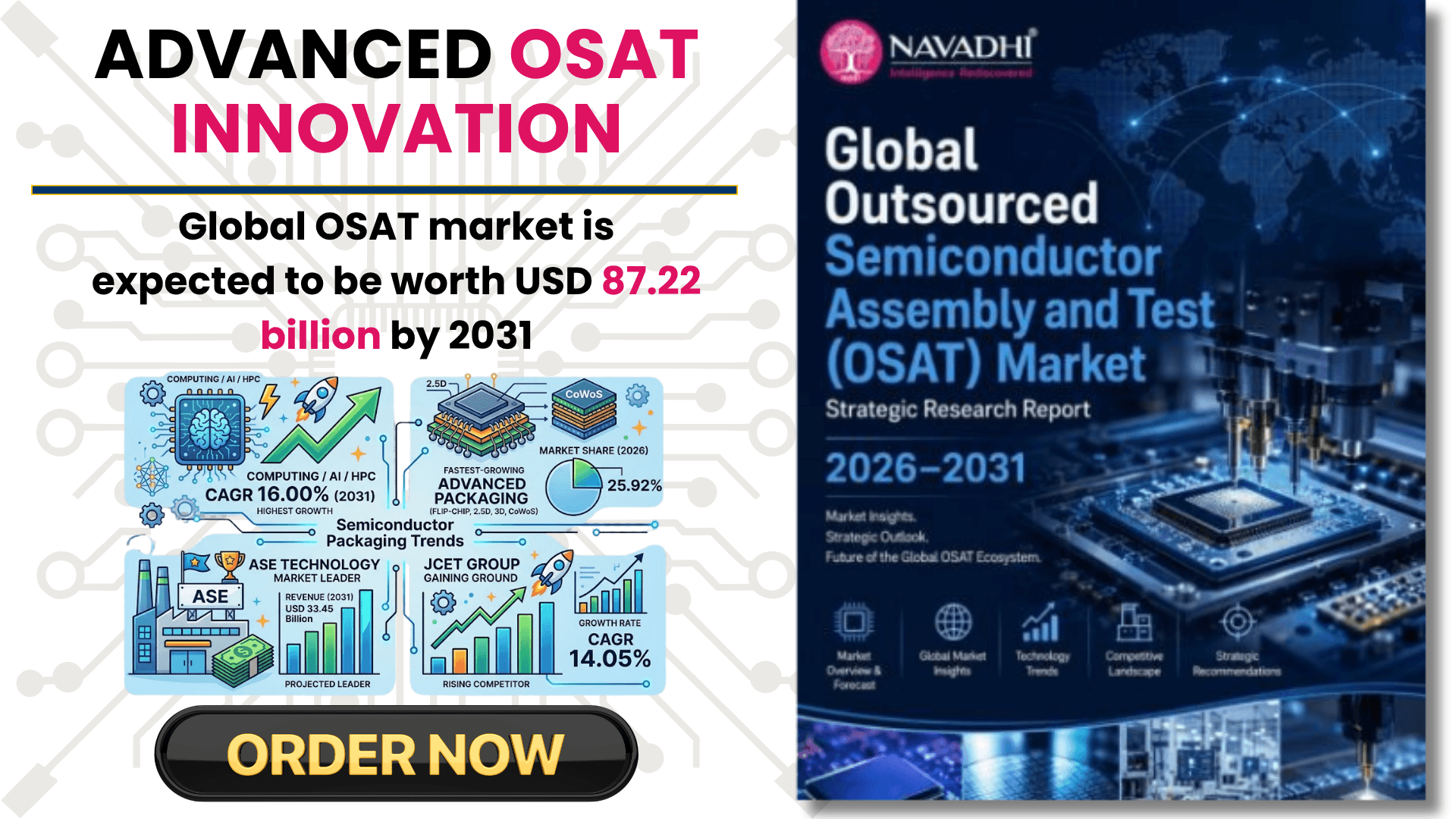

According to the NAVADHI Market Research "Global Outsourced Semiconductor Assembly and Test (OSAT) Market Strategic Research Report 2026-2031" published in May 2026, the global OSAT market was valued at USD 52.00 billion in 2025 and is projected to grow at a CAGR of 9.00% between 2026 and 2031, reaching USD 87.22 billion by 2031. This substantial growth is primarily propelled by a structural shift toward advanced silicon integration alongside the rapid expansion of the "AI-Foundry" ecosystem. Furthermore, this rising market momentum is mirrored in pricing power, with the industry's Average Selling Price (ASP) Index projected to climb from a base of 100 in 2025 up to 116 by 2031.

In past OSAT landscape was shaped by two opposing forces: sluggish recovery in traditional end markets (smartphones, consumer electronics, automotive, industrial) that constrained volume growth for established players; and explosive AI-driven demand for advanced packaging technologies (CoWoS, HBM stacking, chiplet integration, 2.5D/3D packaging) that created high-growth pockets within the overall flat market. ASE Technology maintained dominance with USD 18.54 billion in revenue and 44.6% market share within the top 10 — a concentration ratio unmatched in any comparable manufacturing services sector. US-listed Amkor held second place at USD 6.32 billion (-2.8%). The most significant structural development was the surge of Chinese OSATs: JCET grew 19.3% to USD 5.0 billion, HT-Tech grew 26% to USD 2.01 billion, and combined Chinese OSAT revenue grew at multiples of the overall market rate — driven by domestic semiconductor localisation policy, government investment funds, and the retreat of Western and Taiwanese competitors from Chinese customer relationships under US-China technology restrictions.

The OSAT industry is at an inflection point driven by advanced packaging technology. Traditional wire-bond and flip-chip packaging — which dominated the industry for 30 years — is being supplemented and in high-value applications replaced by a new generation of packaging technologies: CoWoS (Chip-on-Wafer-on-Substrate) for AI GPU integration, HBM (High Bandwidth Memory) stacking via through-silicon vias (TSV), fan-out wafer-level packaging (FO-WLP) for 5G modems and wearable SiPs, and chiplet-based heterogeneous integration that enables disaggregating complex monolithic chips into smaller specialised dies combined in a single package. These advanced packaging technologies carry ASP premiums of 3-10× over traditional packaging, and the companies that lead in their implementation — ASE, Amkor, JCET — are commanding the most strategically important customer relationships in the AI infrastructure buildout.

Top 10 OSAT Companies - Rankings

|

# |

Company |

HQ |

FY2024 Revenue |

YoY |

Mkt Share |

|

#1 |

ASE Technology |

Kaohsiung |

USD 18.54B FY2024 |

Essentially flat / marginal decline |

of top-10 OSAT market |

|

#2 |

Amkor Technology |

Tempe |

USD 6.32B FY2024 |

-2.8% (automotive/industrial weakness; computing record) |

of top-10 OSAT market |

|

#3 |

JCET Group |

Jiangyin |

USD 5.00B FY2024 |

+19.3% — fastest-growing top-3 OSAT globally |

of top-10 OSAT market; largest OSAT in mainland China |

|

#4 |

Tongfu (TFME) |

Nantong |

USD 3.32B FY2024 |

+5.6% |

of top-10 OSAT market |

|

#5 |

Powertech Technology |

Hsinchu Science Park |

USD 2.28B FY2024 |

+1% (lackluster; memory market recovery partial) |

of top-10 OSAT market |

|

#6 |

HT-Tech (Huatian) |

Tianshui |

USD 2.01B FY2024 |

+26% — highest growth rate in top 10 |

of top-10 OSAT market; fastest-growing top-10 OSAT |

|

#7 |

WiseRoad / UTAC |

Singapore (UTAC operations); Beijing |

USD 1.56B FY2024 |

+5% |

of top-10 OSAT market |

|

#8 |

Hana Micron |

Cheongju |

USD 920M FY2024 |

+23.7% — second-highest growth in top 10 |

of top-10 OSAT market |

|

#9 |

KYEC |

Zhubei |

USD 910M FY2024 |

-14.5% (KLTech subsidiary sale impact) |

of top-10 OSAT market |

|

#10 |

ChipMOS |

Hsinchu Science Park |

USD 710M FY2024 |

+3.1% |

of top-10 OSAT market |

Source: Global Outsourced Semiconductor Assembly and Test (OSAT) Market Strategic Research Report 2026-2031. All revenue figures in USD. Note: WiseRoad/UTAC combined reporting reflects acquisition structure. KYEC decline due to KLTech subsidiary divestiture — core business healthy. ChipMOS dual-listed NASDAQ/TWSE.

Global OSAT Market Key Statistics

- Combined top-10 OSAT revenue (2024): USD 41.56 billion (+3% YoY) — Source: NAVADHI Global OSAT Report, May 2026

- ASE Technology: USD 18.54B revenue; 44.6% share of top-10 — world's largest OSAT by a dominant margin; NT$595.4B reported in local currency

- Chinese OSAT surge: JCET +19.3%, HT-Tech +26%, combined Chinese top-3 OSATs growing at 3-8× the overall market rate — driven by domestic localisation policy and government investment

- AI impact: CoWoS advanced packaging testing (KYEC), HBM memory packaging (Powertech, Hana Micron), SiP for AI edge devices (ASE, Amkor) are the primary AI-driven growth vectors within OSAT

- Advanced packaging market share growing: Fan-out WLP, 2.5D interposer, chiplet integration, and HBM stacking collectively growing from ~15% of OSAT revenue in 2020 to estimated 25-30% by 2026

- US-China tech conflict reshaping customer allocation: US/EU chip companies diversifying OSAT relationships away from China-based OSATs; Amkor Vietnam, UTAC Southeast Asia, and PTI Taiwan benefit

- CHIPS Act and sovereign packaging: US CHIPS Act funding Amkor Arizona facility; EU Chips Act supporting Bosch, Infineon, STMicro backend investments; reshoring OSAT manufacturing to US and Europe

- Memory packaging boom: SK Hynix HBM dominance (NVIDIA H100/H200 supply) creating secondary demand for memory DRAM packaging at Hana Micron and PTI

- Test market outgrowing packaging: NAVADHI forecasts testing CAGR of 10.35% vs. packaging's lower rate through 2031 — AI chips require 3-10× longer test times than standard logic ICs

- Display driver IC (DDIC) segment: ChipMOS COF packaging for automotive displays (EV cockpits), OLED smartphones, and foldable phones driving stable niche growth

- Chiplet heterogeneous integration: AMD MCM (Tongfu), TSMC CoWoS (KYEC testing), Intel Foveros — chiplet packaging becoming the dominant advanced logic packaging paradigm

- OSAT market size context: Backend semiconductor services represent approximately 20-25% of total semiconductor industry revenue; total global semiconductor market ~USD 600B in 2024

Company Profiles

#1 - ASE Technology Holding Co., Ltd. (NYSE: ASX / TWSE: 3711)

ASE Technology Holding Co., Ltd. (NYSE: ASX; TWSE: 3711) is the world's largest outsourced semiconductor assembly and test company — and by a margin that no competitor is remotely close to challenging in the near term. Headquartered in Kaohsiung, Taiwan, ASE was founded in 1984 by Richard Chang and Jason Chang. The 2018 merger with SPIL (Siliconware Precision Industries) — completed after a multi-year contested acquisition — created a combined entity with nearly double the capacity of its nearest competitor and cemented ASE's structural dominance of the global OSAT market. ASE generated USD 18.54 billion in FY2024 revenue, representing 44.6% of the combined revenue of the world's top 10 OSAT companies — a concentration ratio unmatched in any comparable manufacturing services sector.

ASE's competitive architecture spans the complete semiconductor backend value chain. Its packaging services cover every major technology node: wire bonding, flip-chip BGA, wafer-level chip-scale packaging (WL-CSP), fan-out wafer-level packaging (FO-WLP), System-in-Package (SiP), 2.5D interposer packaging, and emerging 3D stacking. Its VIPack platform — Vertical Integration Package — is ASE's branded advanced packaging ecosystem targeting the AI, HPC, and 5G markets where chiplet integration and heterogeneous packaging are replacing monolithic chip designs. The Universal Scientific Industrial (USI) subsidiary provides electronic manufacturing services (EMS), giving ASE a revenue stream beyond pure OSAT that shields it from semiconductor cycle downturns. In FY2024, ASE faced headwinds from sluggish recovery in smartphones, consumer electronics, automotive, and industrial sectors, while AI-related orders provided a partial offset. The company is investing aggressively in CoWoS-adjacent packaging capacity — critical for NVIDIA AI GPU production — and expanding its Penang, Malaysia facility as a geographically diversified alternative to Taiwan-concentrated manufacturing.

Quick Facts

- HQ: Kaohsiung, Taiwan

- FY2024 Revenue: USD 18.54B FY2024; NT$595.4B reported; 44.6% share of top-10 OSAT market

- Key Services: IC packaging (flip-chip, BGA, SiP, fan-out WLP, 2.5D/3D); IC testing (wafer probe, final test, burn-in); EMS (electronic manufacturing services via USI subsidiary); substrate manufacturing

- Key Customers: Apple (SiP for AirPods, Apple Watch), Qualcomm, MediaTek, AMD, NVIDIA, Broadcom, NXP

- 2024–2026 Update: World's largest OSAT by a dominant margin (44.6% of top-10); VIPack platform for AI/HPC advanced packaging; CoWoS-adjacent packaging for AI GPUs; new 2.5D interposer capacity in Kaohsiung; Penang Malaysia expansion; USI EMS driving non-semiconductor revenue; 2025 guidance cautious on automotive/industrial but positive on AI/communications.

#2 - Amkor Technology, Inc. (NASDAQ: AMKR)

Amkor Technology, Inc. (NASDAQ: AMKR) is the world's second-largest OSAT company and the largest US-listed pure-play semiconductor packaging and test company. Founded in 1968 by James Kim and headquartered in Tempe, Arizona, Amkor is distinguished from its Asian competitors by its US corporate identity and its uniquely deep relationship with Apple — which relies on Amkor as the primary manufacturer of the System-in-Package (SiP) modules inside every AirPod, Apple Watch, and HomePod. This Apple relationship creates both extraordinary revenue concentration risk (Apple historically represents 25-35% of Amkor's revenue) and extraordinary technology access, as Apple's SiP requirements push the frontier of advanced packaging miniaturisation.

Amkor's FY2024 decline of 2.8% to USD 6.32 billion was driven by two segments: automotive (prolonged inventory corrections as vehicle production slowed globally) and communications (pricing pressure in Asia). However, the computing segment — driven by ARM-based PCs and AI accelerator devices — reached a record in 2024, demonstrating Amkor's growing exposure to the AI infrastructure buildout. Strategic priorities for 2025-2026 include: ramping the new Vietnam facility (USD 1.6 billion total investment) serving Southeast Asian electronics manufacturing; completing the Arizona advanced packaging facility receiving CHIPS Act incentive funding, which will be Amkor's first US manufacturing site since 2000 and positioned as a sovereign supply chain asset for US defense and automotive customers; and the joint venture with GlobalFoundries in Portugal targeting European automotive and industrial semiconductor customers seeking EU-domiciled backend manufacturing.

Quick Facts

- HQ: Tempe, Arizona, USA

- FY2024 Revenue: USD 6.32B FY2024 (-2.8% YoY); net income USD 354M; 15.2% share of top-10 OSAT market

- Key Services: Advanced SiP (Apple); flip-chip BGA; fan-out panel-level packaging; wafer-level packaging; MEMS packaging; power packaging; RF modules; semiconductor testing (wafer probe, final test, burn-in)

- Key Customers: Apple (primary — iPhone SiP, wearables), Qualcomm, Samsung, SK Hynix, automotive tier-1s (Bosch, Continental), Texas Instruments, Skyworks

- 2024–2026 Update: FY2024 USD 6.32B (-2.8%); record Advanced SiP revenue (Apple-driven); new Vietnam facility ramped 2024; Arizona advanced packaging facility (CHIPS Act funded) under construction; joint Portugal project with GlobalFoundries for European automotive customers; computing end market grew to record in 2024; 2025 guidance improvement driven by AI/computing.

#3 - JCET Group Co., Ltd. (江苏长电科技) (SSE: 600584)

JCET Group Co., Ltd. (SSE: 600584) is mainland China's largest semiconductor packaging and test company and the world's third-largest OSAT overall — a remarkable achievement for a company that was a domestic Chinese mid-tier player just a decade ago. Founded in 1972 in Jiangyin, Jiangsu Province, JCET's transformation into a global player was catalysed by the 2015 acquisition of Stats ChipPAC — a Singapore-headquartered OSAT with global operations — for approximately USD 780 million, funded in part by China's national semiconductor investment fund. This acquisition gave JCET instant access to advanced fan-out wafer-level packaging technology (eWLB), international customer relationships, and non-China manufacturing locations in Singapore, South Korea, and Malaysia.

JCET's FY2024 performance was exceptional: 19.3% revenue growth to USD 5.0 billion, driven by the convergence of three tailwinds — recovering consumer electronics demand globally (smartphone IC inventory clearance from 2023), Chinese domestic semiconductor localisation policy creating captive demand from Chinese fabless customers, and new platform ramps in AI PCs and mid-range smartphones. JCET's eWLB (embedded Wafer Level Ball Grid Array) technology — the fan-out packaging platform developed by Infineon and licensed to JCET through the Stats ChipPAC acquisition — is the foundational technology for packaging 5G modem chips and AI PC processors. China's 'Big Fund' (National Integrated Circuit Industry Investment Fund) and local Jiangsu government investment are supporting a CNY 10 billion+ advanced packaging campus expansion in Wuxi that will position JCET as China's most advanced packaging facility by 2027.

Quick Facts

- HQ: Jiangyin, Jiangsu, China

- FY2024 Revenue: USD 5.00B FY2024 (+19.3% YoY); 12% share of top-10 OSAT market; largest OSAT in mainland China

- Key Services: IC packaging (eWLB fan-out, SiP, flip-chip, wire bond, QFN/DFN, stacked packages); IC testing; wafer bumping; advanced packaging (chiplets, 2.5D); substrate manufacturing

- Key Customers: Qualcomm, MediaTek, Hisilicon/Huawei, Unisoc, Samsung, NXP, Chinese fabless ecosystem (AI chips, 5G modems)

- 2024–2026 Update: FY2024 USD 5.0B (+19.3%) — strongest growth of any top-3 OSAT; benefiting from China domestic semiconductor localization policy; SiP and eWLB capacity expansion; chiplet advanced packaging R&D in Jiangyin; Singapore facility (formerly Stats ChipPAC) serving global customers outside China tariff exposure; new Wuxi advanced packaging campus investment CNY 10B+

#4 -Tongfu Microelectronics Co., Ltd. (TFME / 通富微电) (SZSE: 002156)

Tongfu Microelectronics Co., Ltd. (SZSE: 002156), commonly known as TFME or Tongfu, is the world's fourth-largest OSAT and China's second-largest behind JCET. Headquartered in Nantong, Jiangsu Province, TFME is most strategically important for its role as AMD's primary packaging partner for advanced flip-chip and multi-chip module (MCM) packaging of AMD EPYC server CPUs, Ryzen desktop/laptop processors, and Radeon graphics processors. This AMD relationship — which developed following AMD's strategic partnership with Chinese investors in 2016 — gives Tongfu access to the most technically demanding flip-chip and MCM packaging requirements in the industry: AMD's MCM package (multi-chip module combining separate compute dies and I/O dies connected via high-bandwidth interconnects) represents the frontier of advanced heterogeneous integration.

TFME's FY2024 revenue growth of 5.6% to USD 3.32 billion was driven primarily by the communications and consumer electronics rebound, combined with the stability provided by its AMD packaging volume. The retreat of some foreign OSAT competitors from the Chinese domestic market — driven by US-China technology restrictions and supply chain diversification pressures — has opened additional Chinese fabless customer opportunities for TFME. The company is investing in advanced packaging capabilities at its Hefei facility to handle AMD's increasingly complex MCM and chiplet packaging requirements, and is developing its own chiplet integration capabilities that could position it as a leading provider of 2.5D/3D heterogeneous integration services to Chinese AI chip designers (companies like Cambricon, Biren, Moore Threads) that are scaling aggressively despite US export restrictions on advanced GPUs.

Quick Facts

- HQ: Nantong, Jiangsu, China

- FY2024 Revenue: USD 3.32B FY2024 (+5.6% YoY); 8% share of top-10 OSAT market

- Key Services: IC packaging (wire bond, flip-chip BGA, wafer-level CSP, SiP); IC testing; AMD CPU/GPU packaging (primary differentiator); MCM (multi-chip module) packaging for HPC

- Key Customers: AMD (primary — CPU and GPU flip-chip BGA packaging), MediaTek, domestic Chinese chipmakers

- 2024–2026 Update: FY2024 USD 3.32B (+5.6%); AMD packaging relationship core competitive moat — packages Ryzen, EPYC, and Radeon processors; expanding Hefei plant capacity for AMD MCM packaging; Suzhou facility for communications ICs; benefiting from retreat of foreign OSATs from China under US-China tech conflict; pursuing advanced chiplet packaging capability

#5 - Powertech Technology Inc. (PTI / 力成科技) (TWSE: 6239)

Powertech Technology Inc. (TWSE: 6239) is the world's fifth-largest OSAT and the leading specialist in memory IC packaging — a distinct market segment from logic IC packaging that requires specific process expertise for DRAM, NAND Flash, and NOR Flash packaging. Headquartered in Hsinchu Science Park, Taiwan, PTI was founded in 1997 and has built a deep specialisation in memory packaging technologies including Thin Small Outline Package (TSOP), Ball Grid Array (BGA), multi-chip package (MCP), Package-on-Package (PoP), and increasingly High Bandwidth Memory (HBM) stacking. Its customer base is anchored by the three global DRAM leaders — Samsung, SK Hynix, and Micron — all of whom outsource portions of their memory packaging requirements to PTI.

PTI's FY2024 performance of +1% growth to USD 2.28 billion reflected the partial recovery of the memory semiconductor market from the severe 2022-2023 downturn. Standard DRAM and NAND Flash pricing improved in 2024 but remained below peak levels, limiting the volume uplift to PTI's core business. The most strategically important development for PTI's long-term positioning is the HBM (High Bandwidth Memory) market: SK Hynix's HBM3E (used in NVIDIA H100 and H200 AI GPUs) and Samsung's HBM3E production require advanced through-silicon via (TSV) stacking of multiple DRAM dies — a process at the frontier of memory packaging. PTI's TSV capability and its established relationships with all three memory majors position it to capture a portion of the rapidly growing HBM packaging market, which could be worth USD 5-10 billion by 2027 as AI GPU production scales.

Quick Facts

- HQ: Hsinchu Science Park, Taiwan

- FY2024 Revenue: USD 2.28B FY2024 (+1% YoY); 5.5% share of top-10 OSAT market

- Key Services: Memory IC packaging (DRAM, NAND Flash, NOR Flash — primary specialisation); logic IC packaging (wire bond, flip-chip, PoP); wafer-level packaging; IC testing (memory test); chip-on-board

- Key Customers: Samsung (DRAM/NAND packaging), SK Hynix, Micron, MediaTek (logic ICs), Nanya Technology

- 2024–2026 Update: FY2024 USD 2.28B (+1%); memory market recovery partial in 2024 — HBM demand growing but standard DRAM/NAND pricing depressed; exploring HBM packaging services as SK Hynix and Samsung ramp HBM3E for AI GPUs; Longteng (Taichung) facility expansion; DRAM on-package stacking for HPC applications developing

#6 - Huatian Technology / HT-Tech (天水华天科技) (SZSE: 002185)

Huatian Technology (SZSE: 002185), operating commercially as HT-Tech, is China's third-largest OSAT and the fastest-growing major packaging company in the world in 2024, with 26% revenue growth to USD 2.01 billion — the highest growth rate of any top-10 OSAT globally. Headquartered in Tianshui, Gansu Province — an unusual inland location for a semiconductor manufacturer, reflecting the company's origins in the Chinese military-industrial infrastructure of the 1960s — HT-Tech has grown from a state-owned enterprise into a publicly listed national semiconductor champion. Its acquisition of Flipchip Unisem — a Malaysian OSAT subsidiary of Unisem Group — gave it international manufacturing capability, particularly for automotive-grade flip-chip packaging that meets AEC-Q100 reliability standards required by global automotive OEMs.

HT-Tech's 26% revenue surge in 2024 reflects a virtuous convergence: China's domestic semiconductor industry is expanding across automotive, IoT, power management, and AI edge computing applications; the localisation policy pushing Chinese OEMs to use Chinese semiconductor suppliers is creating structural demand for domestic packaging services; and HT-Tech's investment in advanced packaging capabilities (SiP, WLP, TSV) is positioning it to capture high-value orders that previously went to ASE or Amkor. The Flipchip Unisem integration provides automotive packaging credibility — a segment where reliability certification (AEC-Q100) creates high switching costs — and access to Infineon and Texas Instruments as international customers who specified Unisem's Malaysian facilities before the Huatian acquisition. With continued government support and an expanding domestic chipmaker ecosystem, HT-Tech is on track to breach the USD 3 billion revenue threshold by 2026.

Quick Facts

- HQ: Tianshui, Gansu, China

- FY2024 Revenue: USD 2.01B FY2024 (+26% YoY); 4.8% share of top-10 OSAT market; fastest-growing top-10 OSAT

- Key Services: IC packaging (QFN/DFN, SOP, TO-series power packages, BGA, WLP, SiP); power semiconductor packaging; MEMS packaging; automotive semiconductor packaging; IoT/sensor packaging

- Key Customers: Domestic Chinese chipmakers (automotive, IoT, power management), Infineon (through Flipchip Unisem acquisition), Texas Instruments, international automotive tier-1 suppliers

- 2024–2026 Update: Fastest-growing major OSAT in 2024 (+26%); Flipchip Unisem (Malaysia) acquisition brings automotive-grade packaging capability and international customer access; Kunshan and Xi'an facility expansions; focus on AI, HPC, automotive electronics, and memory; benefiting from China domestic semiconductor localisation across automotive and IoT chip production; SiP and TSV capabilities being developed

#7 - WiseRoad Capital / UTAC Group (Private (WiseRoad Capital — private equity; UTAC — previously listed, now private))

WiseRoad Capital / UTAC Group represents the combination of a Chinese private equity firm (WiseRoad Capital, Beijing) and UTAC Group — a Singapore-headquartered OSAT with operations in Singapore, Thailand, Indonesia, and Malaysia that was originally the Southeast Asian division of United Test and Assembly Center. WiseRoad Capital's acquisition of UTAC gave it control of a geographically diversified OSAT with strong automotive and analog semiconductor packaging capabilities and established relationships with major analog/mixed-signal chip companies (Analog Devices, TI, STMicroelectronics) that value UTAC's automotive-grade reliability qualifications and non-China manufacturing footprint.

The strategic positioning of WiseRoad/UTAC at USD 1.56 billion is complicated by the uncertainty around ownership: as of 2025, reports indicate WiseRoad Capital is considering a sale of UTAC — a potential divestiture that reflects the challenges of managing a high-capital-intensity semiconductor manufacturing business from a private equity perspective without the scale of a strategic operator. UTAC's primary competitive asset is its geographic positioning: with manufacturing in Singapore, Thailand, Indonesia, and Malaysia, UTAC can serve customers seeking non-China packaging capacity — a significant and growing demand category as US and European semiconductor companies diversify supply chains away from China exposure. This positioning becomes more valuable under continued US-China technology restriction escalation.

Quick Facts

- HQ: Singapore (UTAC operations); Beijing, China (WiseRoad Capital)

- FY2024 Revenue: USD 1.56B FY2024 (+5% YoY); 3.7% share of top-10 OSAT market

- Key Services: IC packaging (QFP, QFN, SOP, PDIP, flip-chip, automotive-grade packages); IC testing (final test, burn-in); automotive and industrial semiconductor packaging (AEC-Q100 qualified); analog IC packaging

- Key Customers: Analog Devices, Texas Instruments, STMicroelectronics, automotive semiconductor companies (Infineon, NXP, Renesas customers), industrial IC customers

- 2024–2026 Update: UTAC Group acquired by WiseRoad Capital (Chinese PE) — integration ongoing; WiseRoad reportedly considering sale of UTAC (The Business Times Singapore report, 2025); UTAC Singapore and Thailand facilities provide non-China packaging capacity relevant for US/EU tariff-sensitive customers; automotive packaging AEC-Q100 qualification is primary competitive asset

#8 - Hana Micron Inc. (하나마이크론) (KOSDAQ: 067310)

Hana Micron Inc. (KOSDAQ: 067310) is South Korea's leading independent OSAT company and the world's eighth-largest, specialising in memory semiconductor packaging with a deep strategic relationship with SK Hynix — South Korea's second-largest semiconductor company and the world's leading supplier of HBM (High Bandwidth Memory) for AI GPUs. Founded in 2001 and headquartered in Cheongju, North Chungcheong — adjacent to SK Hynix's primary manufacturing campus in Icheon — Hana Micron has built its business model around being SK Hynix's primary outsourced packaging partner for DRAM and NAND memory products.

Hana Micron's 23.7% revenue growth in FY2024 to USD 920 million is directly linked to SK Hynix's extraordinary success in the HBM market: as SK Hynix became the dominant supplier of HBM3 and HBM3E to NVIDIA (used in H100 and H200 AI GPUs), production of standard DRAM for PC, server, and mobile applications was partially outsourced to Hana Micron to free SK Hynix's in-house capacity for the higher-margin HBM. This 'trickle-down' benefit from SK Hynix's premium mix shift is a structural advantage for Hana Micron that is expected to persist as long as AI GPU demand drives HBM demand. Hana Micron is also expanding into automotive memory packaging (LPDDR5 for ADAS systems, eMMC for automotive infotainment) and building a Vietnam manufacturing facility in Da Nang as a geographically diversified packaging platform.

Quick Facts

- HQ: Cheongju, North Chungcheong, South Korea

- FY2024 Revenue: USD 920M FY2024 (+23.7% YoY); 2.2% share of top-10 OSAT market

- Key Services: Memory IC packaging (DRAM, NAND, LPDRAM for mobile); NAND module assembly; SSD packaging; eMCP (embedded multi-chip package); automotive memory packaging

- Key Customers: SK Hynix (primary — dominant relationship), Samsung, Kioxia (NAND flash), automotive customers (memory for ADAS/infotainment)

- 2024–2026 Update: FY2024 USD 920M (+23.7%); SK Hynix primary customer relationship driving strong memory packaging demand; SK Hynix HBM success (HBM3E = dominant AI GPU memory) benefiting Hana Micron through increased DRAM packaging volumes; expanding Vietnam operations (Da Nang facility) for supply chain diversification; HBM-adjacent packaging services developing

#9 - King Yuan Electronics Co., Ltd. (KYEC / 京元電子) (TWSE: 2449)

King Yuan Electronics Co., Ltd. (TWSE: 2449) is the world's largest independent pure-play semiconductor testing services company — a distinction that sets it apart from all other OSATs in this ranking that combine packaging with testing. Founded in 1987 and headquartered in Zhubei, Hsinchu County, KYEC generates virtually all of its revenue from semiconductor testing: wafer probing, final IC testing, burn-in, and system-level test — without the capital-intensive wafer dicing, wire bonding, and package assembly processes that define most OSATs. This focused model allows KYEC to invest deeply in test expertise, automated test equipment (ATE) hardware, and test program development.

KYEC's FY2024 revenue decline of 14.5% to USD 910 million was primarily driven by the divestiture of its KLTech subsidiary — a one-time structural event rather than a reflection of core business health. The underlying test business was actually strengthened in 2024 by a powerful new demand driver: AI chip testing. TSMC's CoWoS (Chip-on-Wafer-on-Substrate) advanced packages — used for NVIDIA H100, H200, and B100 AI GPUs — require sophisticated post-packaging testing that goes beyond standard IC test, including interconnect testing across chiplet boundaries, high-power burn-in at elevated temperatures, and system-level validation. KYEC has been identified by NAVADHI as a key beneficiary of 'growing CoWoS testing demand' — a revenue stream that is expected to scale significantly as AI GPU production volumes increase through 2025-2027.

Quick Facts

- HQ: Zhubei, Hsinchu County, Taiwan

- FY2024 Revenue: USD 910M FY2024 (-14.5% YoY); 2.2% share of top-10 OSAT market

- Key Services: Semiconductor testing (wafer probing, final test, burn-in — pure-play test specialist); CoWoS testing for AI chips; GPU/HPC chip burn-in and functional test; system-level test (SLT); high-temperature burn-in for reliability screening

- Key Customers: TSMC (CoWoS wafer-level package testing), NVIDIA, AMD, MediaTek, Qualcomm (test services for leading-edge process nodes)

- 2024–2026 Update: FY2024 USD 910M (-14.5% — largely due to KLTech subsidiary divestiture, not core business decline); CoWoS AI chip testing growing strongly — KYEC is a key test partner for TSMC's CoWoS-packaged AI GPUs; burn-in testing for AI accelerators requiring extended test times; pure-play test focus differentiates from packaging-led OSATs; 2025 outlook positive driven by AI chip test demand

#10 - ChipMOS TECHNOLOGIES INC. (南茂科技) (NASDAQ: IMOS / TWSE: 8150)

ChipMOS TECHNOLOGIES INC. (NASDAQ: IMOS; TWSE: 8150) is the world's #10 OSAT and a highly specialised packaging and testing company that occupies a unique niche: it is the global leader in Chip-on-Film (COF) packaging for display driver integrated circuits (DDICs), giving it a dominant position in a segment that most OSATs do not serve. Founded in 1997 in Hsinchu Science Park, Taiwan, ChipMOS has built a business model around the two highest-volume display technologies — LCD and OLED — whose driver ICs require COF or COG packaging that is distinct from the flip-chip and wire-bond packaging used for most logic and memory chips.

ChipMOS's FY2024 revenue growth of 3.1% to USD 710 million was driven by automotive display demand — specifically the increasing adoption of larger, higher-resolution instrument cluster and centre console display panels in electric vehicles and premium ICE vehicles, each of which requires multiple display driver ICs in COF packages. The OLED trend is a structural growth driver: as smartphones transition from LCD to OLED displays globally (now >60% of new smartphone shipments), demand for OLED-grade DDIC packaging — which requires higher precision COF than LCD packaging — is growing. The foldable smartphone category (Samsung Galaxy Z Fold/Flip, Huawei Mate X) uses extremely demanding ultra-thin flexible COF packages that carry significant ASP premiums. ChipMOS also operates a DRAM and NOR Flash packaging and testing business that provides revenue diversification beyond the display IC niche.

Quick Facts

- HQ: Hsinchu Science Park, Taiwan

- FY2024 Revenue: USD 710M FY2024 (+3.1% YoY); 1.7% share of top-10 OSAT market

- Key Services: Display Driver IC packaging (COF — Chip on Film, COG — Chip on Glass, TCP); LCD/OLED driver IC testing; DDIC (display driver IC) packaging — global market leader; memory IC packaging and testing (DRAM, NOR Flash)

- Key Customers: Novatek Microelectronics (primary), Himax Technologies, Raydium Semiconductor, Ilitek, automotive display suppliers (via tier-1 IC designers)

- 2024–2026 Update: FY2024 USD 710M (+3.1%); LCD driver IC demand stable from automotive displays (instrument clusters, infotainment); OLED driver IC growing as smartphone display upgrades to OLED accelerate; COF packaging for foldable phone display drivers (Samsung Galaxy Z-fold, Huawei Mate XT); automotive DDIC demand growing as EV cockpits adopt larger/more display screens; DRAM test services stable

Key Industry Trends

1. AI and HPC - The Defining Growth Driver for Advanced Packaging

Artificial intelligence and high-performance computing are fundamentally reshaping the OSAT industry. NVIDIA's H100, H200, and B100 AI GPUs are among the most technically demanding semiconductor products ever manufactured — each requiring CoWoS (Chip-on-Wafer-on-Substrate) advanced packaging that integrates the GPU die with HBM memory stacks on a silicon interposer, assembled in a single package. This packaging requirement is TSMC-OSAT collaborative work, with KYEC performing a significant portion of the testing. Beyond GPUs, AI is driving demand for advanced SiP (System-in-Package) for AI edge inference chips, HBM stacking for AI memory, and chiplet integration for disaggregated AI processor architectures. The OSAT companies investing in CoWoS-adjacent capabilities, HBM packaging, and chiplet integration are commanding the most strategically valuable customer relationships of the decade.

2. Chinese OSAT Ascendancy - Policy-Backed, Domestically-Fuelled

The 26% growth of HT-Tech, 19.3% growth of JCET, and 5.6% growth of Tongfu collectively represent the most significant competitive shift in the OSAT industry since the 1990s. China's national semiconductor self-sufficiency policy — implemented through the 'Big Fund' (National Integrated Circuit Industry Investment Fund, now in its third phase with CNY 344 billion committed) and provincial investment programmes — is creating captive domestic demand for Chinese OSAT services. Chinese fabless chip designers (HiSilicon/Huawei, Unisoc, Cambricon, Biren, Moore Threads, Zhaoxin) that historically used TSMC for fabrication and ASE/Amkor for packaging are being pushed — and in many cases choosing — to use domestic OSATs for packaging and test. This structural demand reorientation is a multi-decade trend, not a short-term cycle.

3. Geographic Diversification - US, Vietnam, Europe as New OSAT Hubs

The semiconductor packaging industry is experiencing its first significant geographic diversification in 30 years. Amkor's USD 1.6 billion Vietnam facility (ramped 2024) and Arizona advanced packaging plant (CHIPS Act funded, opening 2025-2026) represent the most visible manifestations of the 'China+1' and domestic manufacturing trend. US customers seeking CHIPS Act-compliant supply chains — including US defense contractors, automotive suppliers, and cloud infrastructure providers — are driving demand for domestic or trusted-nation packaging capacity. Similarly, Europe's semiconductor sovereignty agenda is driving OSAT-adjacent investment: Bosch, Infineon, and STMicroelectronics are all building or expanding European backend manufacturing capabilities. Silicon Box received EU approval for a EUR 1.3 billion panel-level packaging plant in Italy.

4. Memory Packaging Renaissance - HBM Driving Premium Mix

High Bandwidth Memory (HBM) is one of the most technically demanding semiconductor products in existence: it requires stacking 8-12 DRAM dies vertically using through-silicon via (TSV) connections, with each die communicating through the via stack at aggregate bandwidths exceeding 1 terabyte per second. SK Hynix's leadership in HBM3 and HBM3E supply to NVIDIA has created extraordinary secondary demand throughout the Korean memory packaging supply chain. Hana Micron's 23.7% growth in FY2024 is the most quantifiable evidence of this trickle-down effect. Powertech Technology's positioning in memory TSV development targets a market that is expected to grow from approximately USD 2-3 billion (2024) to potentially USD 10-15 billion by 2028 as AI server deployments scale globally.

5. Pure-Play Testing Outperforming — AI Chips Require 10× Longer Test Times

The testing segment of the OSAT market is growing faster than the packaging segment — a structural reversal from historical patterns driven by the complexity of AI and HPC chips. A standard mobile application processor might require 15-30 seconds of functional test plus burn-in. An AI GPU like NVIDIA's H100 requires hours of functional test, burn-in at elevated temperatures, and system-level test that validates the complete package across multiple operating modes. This 10-100× increase in test time per chip — combined with production volumes scaling rapidly — is creating acute test capacity constraints. KYEC's position as the world's largest independent test services provider, with CoWoS testing capability and GPU burn-in expertise, gives it structural leverage in the most capacity-constrained segment of the semiconductor supply chain.

Sources

- NAVADHI: Global Outsourced Semiconductor Assembly and Test (OSAT) Market Report' (NAVADHI.com, May 28, 2026) — PRIMARY DATA SOURCE

- Mark Lapedus / Semiconductor Engineering: 'ASE, Amkor Top OSAT Rankings But China Gains Ground' (marklapedus.substack.com, May 13, 2025)

- Mordor Intelligence: 'Outsourced Semiconductor Assembly and Test (OSAT) Market Size Analysis 2031' (mordorintelligence.com, January 2026)

- Amkor Technology: FY2024 Q4 and Full Year Financial Results Press Release (ir.amkor.com, February 10, 2025); AMKR Annual Report 2024

- ASE Technology Holding: FY2024 Annual Results (TWSE filing); NT$595.4B revenue; StockTitan 'ASE Technology Reports Mixed Q4 Results'

- Evertiq: 'Chinese firms gain ground in 2024 top 10 OSAT ranking' (evertiq.com, May 23, 2025)

- Electronics Weekly: 'OSAT top ten grow 3%' (electronicsweekly.com, May 2025)

- Ariat Technology: 'OSAT Companies in 2024: Assembly, Testing, Packaging Types and Market Outlook' (ariat-tech.com, September 2025)

- MatrixBCG: 'Competitive Landscape of Amkor Technology' (matrixbcg.com, September 2025)

- Wikipedia: Huatian Technology (SZSE: 002185) — financial data for HT-Tech

- Custom Market Insights: OSAT Market Size analysis (custommarketinsights.com)

- Anysilicon: 'Top 10 OSAT Companies of 2024 Revealed' (anysilicon.com, May 2025)

Disclaimer

Revenue figures are sourced from NAVADHI's Preliminary Global OSAT Report (May 2026), cross-referenced against company annual reports and industry publications. All figures in USD. Taiwanese and Korean company revenues are converted from local currencies (NTD/KRW) at approximate FY2024 average exchange rates. Chinese company revenues (JCET, TFME, HT-Tech) are from NAVADHI estimates cross-referenced with SSE/SZSE filings. WiseRoad/UTAC revenue is a combined estimate for the group. Market share figures are of combined top-10 OSAT revenue (USD 41.56B), not total global OSAT market

NAVADHI Market Research utilizes real-time data streaming to maintain continuous updates across our commercial report inventory. Please note that public blog content may feature historical or preliminary data points that differ from the real-time metrics available in our paid commercial deliverables.

. © 2026 MarketResearchReports.com · All Rights Reserved.